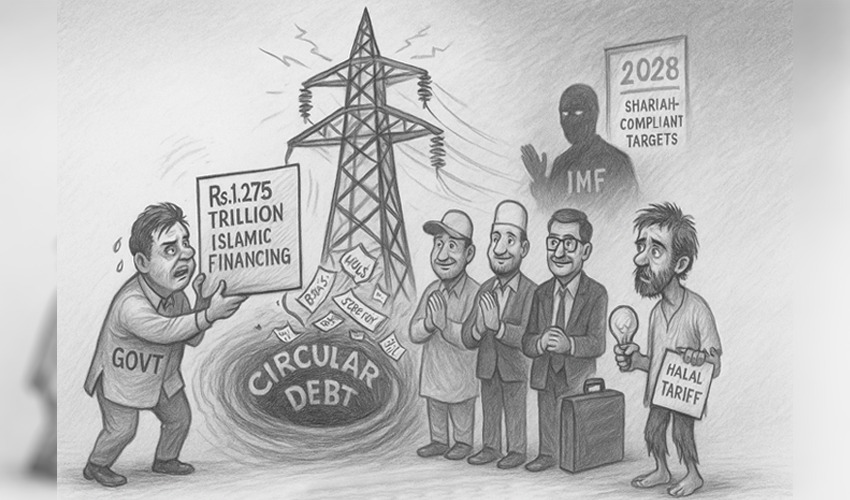

The federal cabinet’s recent nod to secure a Rs1.275 trillion Islamic financing facility from commercial banks to ease the power sector’s debt burden is a well-timed move. The cleanup has been long overdue. That said, it must be understood that this is not a structural correction but a bandage on a pressure sore.

The power sector’s circular debt has been constantly feeding on inefficiencies, subsidies, and unpaid bills like a parasite. Despite massive payments to IPPs every now and then to clear the dues, the numbers refuse to come down, mainly because the system keeps generating more debt than is paid off. The amount payable currently stands at Rs2.4 trillion, which is less than half the total circular debt (exceeding Rs5 trillion) in the energy sector. Still, this new facility is likely to take a lot of pressure off the sector.

Any decision made must not aim at pleasing the ever-watchful IMF but at righting the wrongs that had been going on for decades. Ear-pulling is required at all levels to reverse the situation within loss-making distribution companies.

Turning to Islamic finance is a smart move, as it simultaneously shows how serious the government is about transition toward interest-free banking by 2028. Admittedly, it can be seen as a refinancing operation aimed at reshuffling the debt, but it comes with several smart features. The first one is the concessional pricing of KIBOR minus 0.9% instead of plus 4.5%, which the IPPs are currently charging on arrears. Although it is still debt, the latest facility has been planned to postpone the payments over six years in quarterly instalments. In short, this move may significantly reduce the cost of liabilities. Still, this cost-cutting should not be confused with reform.

Escaping the circular debt trap for good requires a 180-degree policy shift. Any decision made must not aim at pleasing the ever-watchful IMF but at righting the wrongs that had been going on for decades. Ear-pulling is required at all levels to reverse the situation within loss-making distribution companies. Moreover, additional efforts must be made to plug leakages and improve the poor recovery rates. Policymakers need to realize that politically convenient subsidies will only worsen the problem.

The authorities apparently plan to use this liquidity injection to keep the wheels from coming off in the near future, but slaying the circular debt monster is impossible without a proper roadmap for root-level reform. If the status quo is maintained, the circular debt will return with a vengeance.

The IMF approval does not make this the ultimate or permanent solution. After all, the global lender has always been more concerned with numbers than with nuances. The Islamic finance angle does give the impression that the facility is interest-free. Still, it remains a debt that will ultimately be paid by electricity consumers through either tariffs or taxes.

The power sector does not need another loan or temporary relief but proper fixes to its aging infrastructure and outdated regulations. Until that happens, the vicious loop will persist, keeping the dream of sustainable energy out of reach.