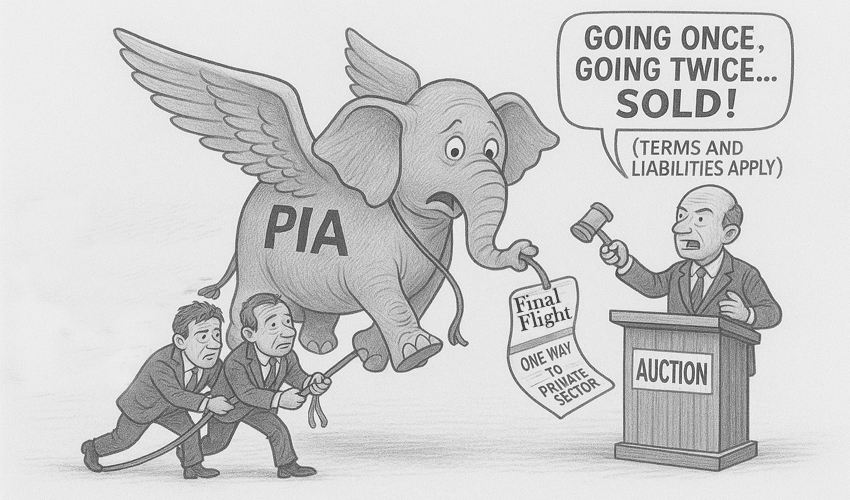

The UK’s decision to open its skies to PIA is a welcome and long-overdue development. The regulatory clearance not only restores the national flag carrier’s access to one of its most important diaspora markets but also adds to the airline’s global legitimacy. However, it would be wrong to treat this development as anything but a runway, for its true destination lies ahead in privatization.

The UK and EU airspaces were shut to the PIA almost five years ago following a tragic Karachi crash in June 2020 and the subsequent global warnings over pilot credential fraud. The crash further shattered the airliner’s reputation and no investor touched the white elephant after that. However, the current scenario has a silver lining. The PIA regained access to the EU last year, and now the UK has cleared Pakistan from its Air Safety List. These developments have changed the equation, bringing the airline’s most valuable commercial routes back in play.

According to estimates from industry analysts, the EU route re-entry alone can add up to $120 million annually to PIA’s revenue. Similarly, the UK corridor is even more lucrative, mainly because of the diaspora of over 1.6 million British Pakistanis. Given the potential of these two routes, the national flag carrier is expected to make substantial revenues, which in turn would boost valuation. From the investors’ point of view, the airliner would now be in a relatively stronger financial position, having route rights to major markets and fewer regulatory liabilities.

The PIA, or its successor, would have to be transformed into a service-oriented and competitive airliner with a modern fleet to yield a handsome return on investment

However, roses do not come without thorns. Despite the lifted bans, the fact remains that the PIA is a high-risk asset. It carries a high debt-to-equity ratio and operates an aging fleet. Moreover, the way workers’ unions have pushed back against privatization in the past is no secret. Although the 6,700-strong workforce has been assured of protection post-privatization, it is unclear how private owners will deliver on all the promises and still revive the loss-making entity. Demands like insulation from political interference, rationalization of workforce costs, and managerial autonomy might put authorities in a difficult position. This particular situation further highlights the need for introducing structural reforms even before the ownership changes hands.

In this context, the government must realize that regulatory clearances have made the PIA more presentable, not healthy. It should therefore resist the temptation to consider this achievement the end of the story. Also, overreliance on diaspora-driven routes would be naive, given that both the UK and EU markets are seasonal and often price-sensitive.

The PIA, or its successor, would have to be transformed into a service-oriented and competitive airliner with a modern fleet to yield a handsome return on investment. The fact that several consortiums are showing interest in acquiring the PIA is a good omen. Now, the next steps in the privatization process need to be transparent. Authorities must ensure that while stakeholders are kept informed, labor concerns are also addressed, but not at the cost of efficiency. If this white elephant is to be sold, it must be done wisely. Until then, the skies are open for the PIA, but its future is still grounded.